Everything You Ought To Find Out About Home Mortgages

Article written by-Mcfadden BreumThe idea of getting a home loan can be rather intimidating. It pays to start the process from a knowledgeable posture in order to make smart choices. The following paragraphs are full of information that you can use to get going in the appropriate direction.

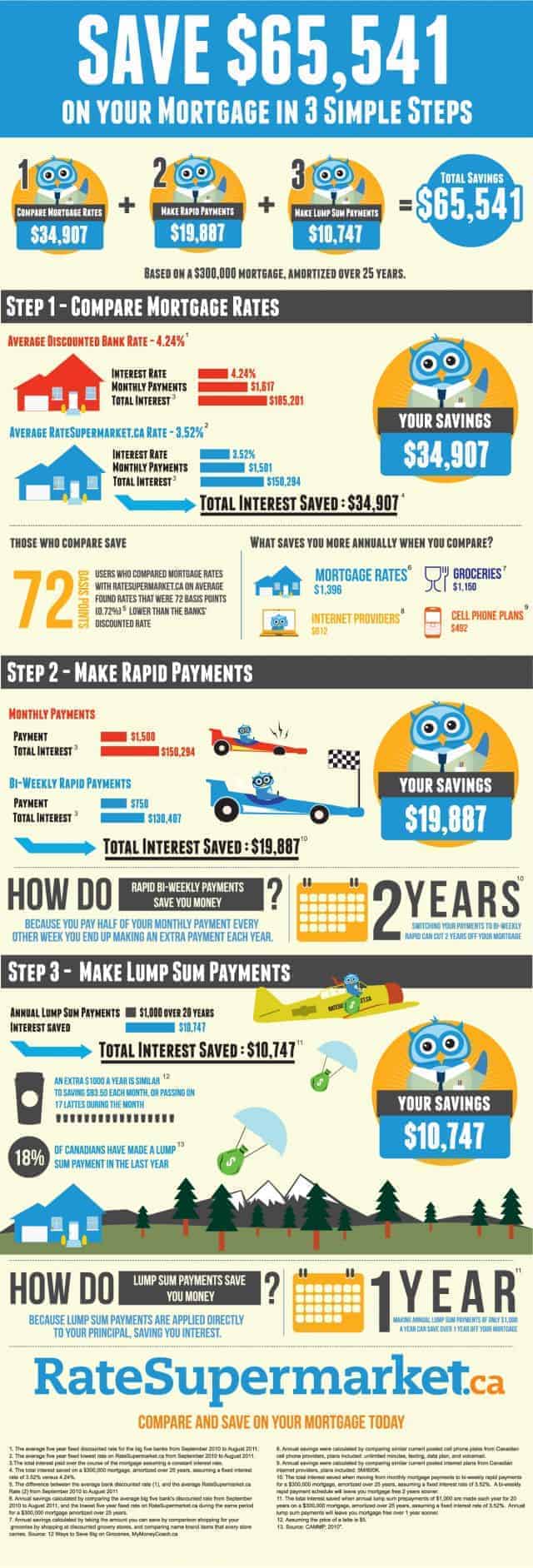

Getting the right mortgage for your needs is not just a matter of comparing mortgage interest rates. When looking at offers from different lending institutions you must also consider fees, points and closing costs. Compare all of these factors from at least three different lenders before you decide which mortgage is best for you.

To make sure that you get the best rate on your mortgage, examine your credit rating report carefully. Lenders will make you an offer based on your credit score, so if there are any problems on your credit report, make sure to resolve them before you shop for a mortgage.

When considering the cost of your mortgage, also think about property taxes and homeowners insurance costs. Sometimes lenders will factor property taxes and insurance payments into your loan calculations but often they do not. You don't want to be surprised when the tax office sends a bill and you learn the cost of required insurance.

Prepare your paperwork before applying for a mortgage. There are many items that a lender will require. These items include the last two or three years worth of tax returns, copies of each of your monthly credit card statements and installment loans. please click the next website page and two months worth of pay stubs are also needed for approval.

Save your money. When you are going to finance a home mortgage, you will need to have some cash for a down payment. The more money you pay down, the lower your payments and interest rates. The down payment goes directly to the principal of the mortgage and is a sum you will not owe yearly interest on.

Pay your credit cards on time if you are considering a home mortgage in the next few years. Your credit score and debt to income ratios will come into play when you go for a home mortgage. If source for this article have multiple late payments or are carrying a lot of debt, you may find the mortgage offers you receive to be poor.

Know that Good Faith estimates are not binding. These estimates are designed to give you a good idea of what your mortgage will cost. It should include title insurance, points, and appraisal fees. Although you can use this information to figure out a budget, lenders are not required to give you a mortgage based on that estimate.

One type of loan that is not normally talked about is an interest only loan. This type of loan allows you to make low monthly payments for a certain period, then the payment amount increases. These loans are generally used to help you get into a home at a low monthly payment.

If you are looking to buy any big ticket items, make sure that you wait until your loan has been closed. Buying large items may give the lender the idea that you are irresponsible and/or overextending yourself and they may worry about your ability to pay them back the money you are trying to borrow.

Do not even consider getting a home mortgage that is only paying the interest. This is the worst possible investment that you can make. The problem is that you are not getting any closer to actually owning your home. Instead, purchase a home that you can afford to pay principle on so that you are truly making a good investment.

Make sure that you have a good amount of savings before you get yourself into a home mortgage contract. There are not certainties when it comes to the economy or job stability. To protect yourself you want to have enough money saved to make your payments for many months in case the worst does occur.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

If you have previously been a renter where maintenance was included in the rent, remember to include it in your budget calculations as a homeowner. A good rule of thumb is to dedicate one, two or even three perecent of the home's market value annually towards maintenance. This should be enough to keep the home up over time.

If you are able to pay a bit more each month, consider 15 and 20-year mortgages. You'll end up paying a lot less interest over the life of your loan. In the long run, you can save thousands over a 30-year loan.

Most financial institutions require that the property taxes and insurance payments be escrowed. This means the extra amount is added onto your monthly mortgage payment and the payments are made by the institution when they are due. This is convenient, but you also give up any interest you could have collected on the money during the year.

Save up lots of money ahead of applying for your mortgage. You will probably have to pay at least three percent down. Paying more is better, though. You need to pay the private mortgage insurance if there are down payments of less than 20%.

Try not to take a mortgage for the entire amount you can afford. If you take the absolute maximum, you won't have much money left as a cushion when your payments come due. If anything unexpected comes up, you may end up in a real pickle if you are spending the most every month.

During the process of obtaining a mortgage loan, submit any requested documents to your mortgage broker or lender as soon as possible. Taking your time to respond to your lender can delay the date of the closing. Delaying the closing date can put you at risk of losing the rate you have locked-in.

Dealing with all the specifics of your home mortgage can be very difficult, especially when you are buying your first home. You need to do some research before you sign the papers to make sure you are getting a good deal. Follow the home mortgage tips listed above for some help with the process.